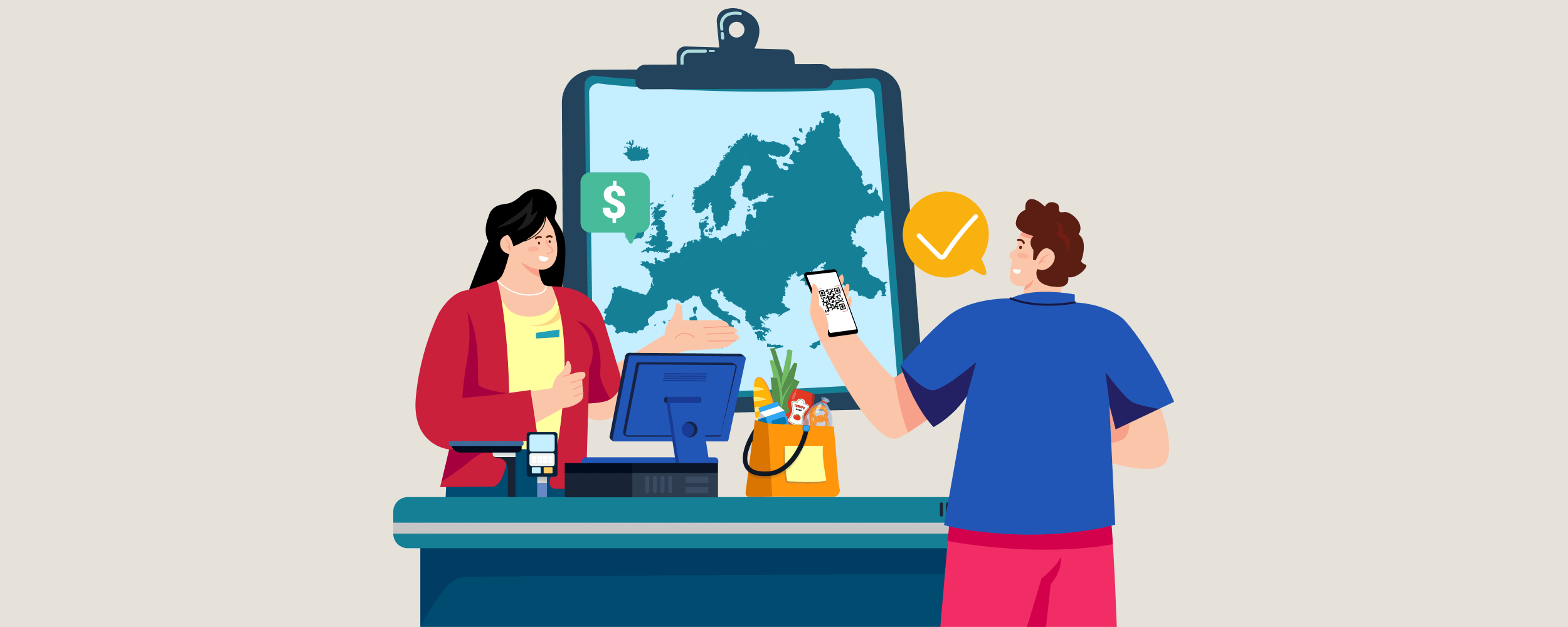

Mobile payment platforms modernise European payment transactions

The pandemic has driven digitalisation, especially in the payment and banking sector. This has created new opportunities, risks and a lot of changes in the entire economy. How the demands of users and the possibilities of mobile payment providers in Europe have developed can be seen in the examples of Credi2, Bluecode, Bitpanda and the European Mobile Payment Systems Association (EMPSA).

They are all major players in the European mobile payment market. Where they want to go and how the payment platforms want to react to the changes of the recent past in order to be successful in the future, they revealed during the Reality Check at the Banking Summit Vienna.

(Almost) all of Europe pays mobile

As an association of the leading mobile payment systems in Europe, EMPSA has set itself the goal of establishing mobile payment in European payment transactions. Whether via Swish in Sweden, Twint in Switzerland or Vipps in Norway - payments are made on Apple and Android devices by scanning a barcode or QR code. The purchase amount is then debited directly from the payer's account. This type of mobile payment is now used by 90 million users across Europe on the platforms of the respective banks. However, this form of mobile payment is not yet so well accepted everywhere in Europe. The German-speaking countries in particular have some catching up to do. Well-functioning European examples should serve as models in Austria and Germany.

Regional differences are also known at the Viennese financing specialist Credi2. While it is common practice in Anglo-Saxon countries to pay for purchases in instalments, this trend is only slowly catching on in the European market.

Faster, simpler, better

In European payment transactions, the signs are pointing to change. One driver of this change is the flexibilisation of the payment industry. One learning that the payment sector could take away from the past two years is that consumers want to be flexible in liquidation. In addition, the need for speed and simplification has also increased. This is also a consequence of the pandemic-related digitisation offensive. Bitpanda now uses ETF sales at the push of a button instead of a complicated trading process. This saves users time and improves the user experience many times over.

Is added value adding value?

The way to the goal for Europe's mobile payment platforms is through the user experience. Only if the services adapt to the needs of the users can they be successful. But how must payment platforms develop or perhaps change in order to meet the wishes of users?

Among other things, Bluecode relies on a mix of sustainability and value-added services. The digital receipt allows customers to suppress the printing of the receipt directly at the POS. Instead, they can request the receipt directly on their mobile phone if they want to keep it. This saves valuable resources as well as a confusing accumulation of receipts that are kept for possible complaints.

Credi2 focuses primarily on added value in terms of simplified user journeys and seamless integration of their services into the world of their customers. "Thanks to the cooperation with Credi2, we can reach even more customers with the Cyberport subscription model for Apple products." René Bittner, Managing Director Purchasing Cyberport (quote from Credi2 website).

More than just pay and manage

Even if you look at individual members of EMPSA, you can see how the trump card of value-added service can be played. In Switzerland, almost every second person uses mobile payment via the Twint platform. In recent years, the number of users has grown from a few hundred thousand to 4.2 million. Part of the success is certainly due to the value-added services. Swiss people use Twint not only to pay, but also to buy insurance or donate to charity, for example.

For Bitpanda, on the other hand, the value-added service is not an additional programme, but a prerequisite that it wants to offer its customers as a digital-first platform. Although users are provided with features such as savings plans, cashback programmes or an automated investment index in addition to the basic functions for investment and trading, Bitpanda does not offer added value at any price - the security of user data always has priority.

Mobile payment for all sizes

Whether for micro-merchants or large banks, mobile payment offers many opportunities in a wide variety of markets in Europe.

Imagine you are passing a small farm shop and want to buy something. Unfortunately, you don't have enough cash on hand, and the nearest rural bank branch is also too far away. The simplest solution for this scenario: a static QR code that allows you to pay quickly and easily via smartphone.

Where does the journey lead?

These and similar use cases can be found all over the world. Why is the potential not being used everywhere?

In and of itself, Austria is also ready for a digital payment offensive. The only thing that seems to be missing in many places is the awareness for modern payment transactions. The business models of the domestic players offer numerous opportunities and possibilities - both for micro-entrepreneurs and for banks.

Moving away from conservation

In the banking sector in particular, however, a lot has to change first. Few applications are as important to smartphone users as banking apps. They are opened regularly, often several times a day, to check the account balance, make transfers or see where the money is going.

This is exactly where the problem lies: nothing more happens in banking apps. And this is despite the fact that the integration of value-added services would not only benefit customers, but also the banks themselves.

For this, the opportunities must be seized and active market cultivation must be pursued instead of stock preservation. The motto must be: Away from the conservative financial institution, towards the modern, digital financial service provider.

More posts

How to...mobile-pocket

If you rely on digital customer loyalty, you rely on mobile-pocket. This is how you get to your loyalty program step by step.

Talent & Technology: Two pitfalls on the road to the financial super app

The race for the financial super app in Europe has started. Those who want to compete need ambitious talent and the appropriate technology.